Investment implications: Position for a broad range of opportunities

We view fixed income investments as broadly appealing over our cyclical horizon, given attractive yields and valuations as well as the potential for resilience across multiple economic scenarios. Such resilience is especially important in the wake of the increase in geopolitical risk and market volatility over the past two years. Because attractive yields can be found in high quality bonds, investors do not need to step down in credit quality.

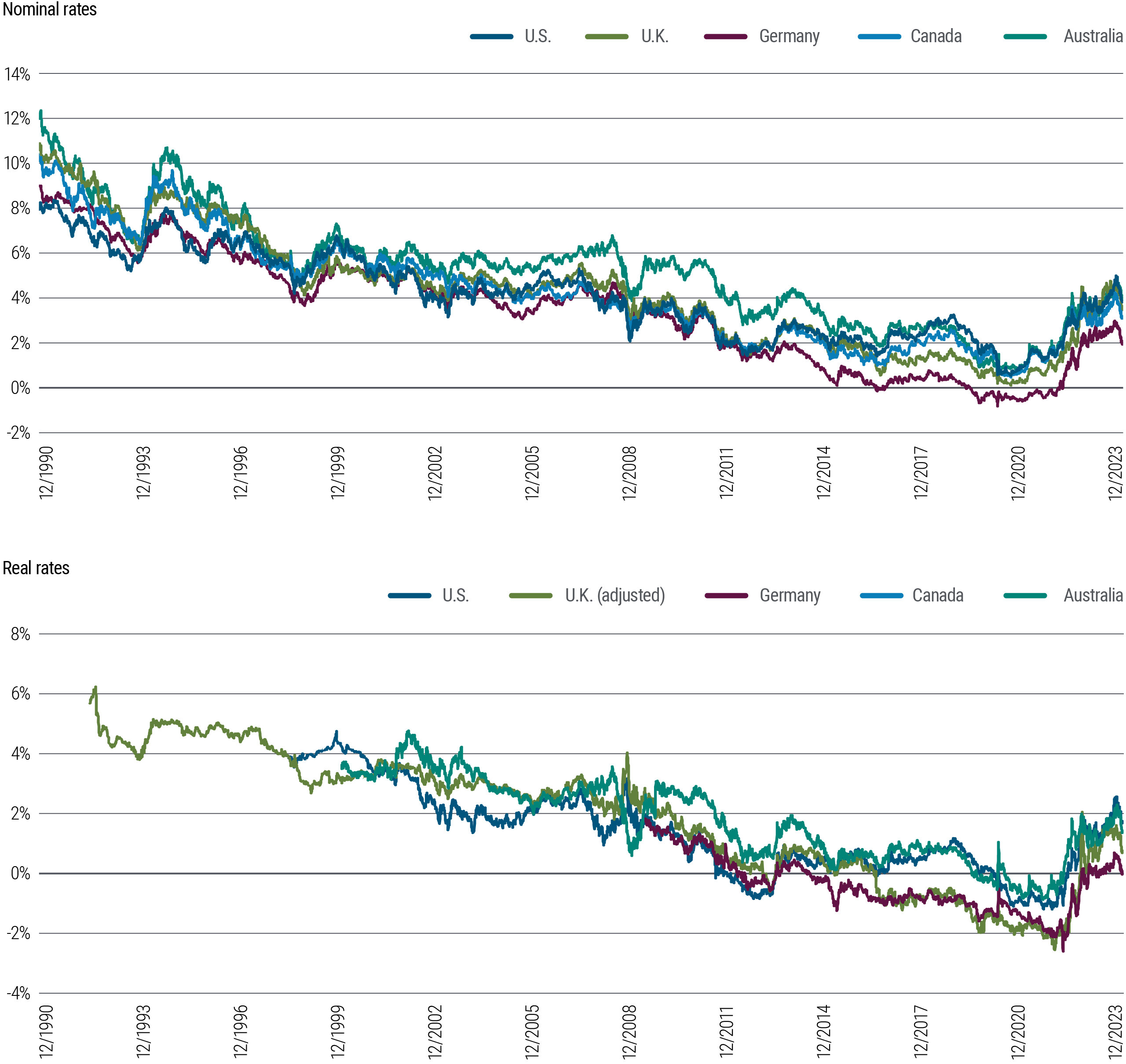

Starting yields, which historically are highly correlated with returns, are still near the highest levels in 15 years, offering both attractive income and potential downside cushion. Inflation-adjusted yields also remain elevated as inflation continues to abate (see Figure 3). We continue to see Treasury Inflation-Protected Securities (TIPS) as a reasonably priced source of inflation protection, should upside inflation risks materialize.

Figure 3: Nominal and real 10-year rates across developed markets

Cash yields remain high but can only be locked in overnight, and they could decline quickly, especially if central banks start cutting policy rates. Investors risk missing out by holding cash too long while trying to time a re-entry into markets.

Because yield curves are unusually flat today, investors don’t need to greatly extend duration – a gauge of sensitivity to changes in interest rates, which is most pronounced in long-dated bonds – to unlock potential value. Intermediate bond maturities can help investors pursue attractive yield along with potential price appreciation should bonds rally, as occurred in late 2023 and as often happens in an economic slowdown.

More symmetrical risks

In our October Cyclical Outlook, “Post Peak,” we argued that global fixed income yields looked both attractive and high relative to the levels we expected to prevail over the cyclical horizon and beyond. After the U.S. had led a third-quarter rise in global yields, we said we expected to maintain overweight duration positions and to increase those with any further rise in yields.

At this point, we don’t see duration extension as a compelling tactical trade. We expect to be broadly neutral on duration after the most recent bond-market rally, which has brought global yields back in line with our expected ranges, and amid the shifting balance of inflation and growth risks. We see those risks as more symmetrical today.

We believe the Fed and other central banks have scope to cut rates aggressively if growth slows. Yet there are also scenarios in which the recent market-based easing of financial conditions has done much of the work for central banks. That easing, alongside continued consumer and corporate-sector strength, could even prompt inflation to flare up again.

This loop between central bank communication, financial conditions, and real economic performance will likely continue. We use scenario planning as part of our risk management process to position for a broad set of macro and market outcomes.

Opportunities across outcomes

We expect fiscal concerns will continue, both in the U.S. and globally. We see potential for further bouts of long-end curve weakness amid anxiety about elevated supply, as occurred in late summer, stemming from the increased bond issuance needed to fund large fiscal deficits. We therefore expect to have a curve-steepening bias in our portfolios, with overweight positions in the 5- to 10-year part of the curve globally, and underweights in the 30-year area.

At current valuations, we continue to find bonds attractive relative to equities (for more, see our latest Asset Allocation Outlook, “Prime Time for Bonds”), while fixed income can continue to offer correlation and diversification benefits in portfolios. Bond returns also tend to be less dependent on a positive economic outcome.

At current valuations, we continue to find bonds attractive.

For example, if current economic conditions persist, bonds have the potential to earn equity-like returns based on today’s starting yield levels. If the economy enters recession, bonds will likely outperform stocks. If inflation revives and central banks need to hike again, both bonds and stocks would likely be challenged, but high starting yields can provide a potential cushion for bonds.

Maintaining a focus on liquidity and portfolio flexibility can allow us to respond to events as the balance between growth and inflation risks evolves. Active management allows us to more nimbly seize upon relative value opportunities as they arise.

Global markets may outperform

After central banks globally raised rates in relative synchrony, their paths ahead are likely to be more differentiated. We continue to see the potential for outperformance of global duration versus the U.S. Our view is based on the relatively higher chance of U.S. economic resilience and the greater downside risks in more rate-sensitive markets, notably, Australia, the U.K., and the eurozone.

We believe opportunities in global bond markets are more attractive than they have been over the past decade. Investors with broad, global platforms can access a diversified set of bond exposures and a variety of sources of potential return.

We expect to focus on more liquid DM overall, given attractive yield levels. We also expect to find good opportunities in emerging markets (EM), both in terms of local and external debt. We expect to be overweight EM foreign exchange, with diversified funding currencies to reduce the correlation between higher-carry EM currencies and global risk assets.

Focus on credit quality

In more credit-oriented markets, we continue to favor U.S. agency mortgage-backed securities as a high quality, liquid form of credit spread in portfolios. We also favor high quality non-agency mortgages, commercial mortgage-backed securities, and asset-backed securities, based on both current valuations and the default-remote properties of these securities given the collateral backing them.

In corporate credit, we favor liquid credit indices, senior financial sector debt, and high quality positions in investment grade and high yield bonds, while exercising greater caution with lower-quality credit and more economically sensitive sectors such as floating-rate bank loans.

The attractive opportunities we see in public markets today contrast with a more nuanced outlook for private credit amid the need to refinance loans in a tougher borrowing environment. Banks are retrenching in the face of liquidity constraints, regulatory restrictions, and cost-structure challenges, as we outlined in our recent publication, “Opportunities in Private Credit: Stepping In as Banks Step Out.”

As the lending community becomes constrained, attractive opportunities in asset-based lending are growing.

In areas such as private credit, commercial real estate, and bank loans, we believe there is an important distinction between the stock of existing assets and the flow of new investment opportunities. The existing stock faces real challenges from higher interest rates and a slowing economy, with a substantial distance remaining to mark private assets to more realistic, market-based price levels, especially in areas with fundamental weakness.

At the same time, the opportunity for flexible capital has become more attractive, as borrowers are in need of creative solutions given a more constrained lending community. Asset-based lending is perhaps the best example of this, where we are seeing bank retrenchment create large-scale liquidity gaps in a variety of forms of consumer and non-consumer lending. This is particularly true in the U.S., as banks seek to sell assets, offload future lending obligations, or exit certain business lines entirely.

Over time, this painful period of adjustment may lead to further opportunities for well-positioned lending platforms to earn proper premiums for less-liquid investments. In turn, we anticipate what could be some of the best lending vintages across private markets since the global financial crisis. Even amid robust activity in corporate direct lending, which has recovered from most of the spread widening that happened since mid-2022, there is still significant need for flexible solutions to complex capital structure problems, many of which could offer equity-like returns in the near- to intermediate-term, in our view.